What Counts as a "Single Item"? Sets and Collections in Probate Valuation

In brief

HMRC's £1,500 threshold for professional probate valuations applies per "single item", but matched sets, pairs, and natural collections are usually valued together as one unit. A pair of Georgian candlesticks worth £900 each will typically count as a single £1,800 set requiring professional valuation. The "natural unit" principle from Duke of Buccleuch v IRC governs how sets are treated, and HMRC's form IHT407 sets out the practical reporting rules.

The £1,500 Threshold in Context

HMRC's guidance on valuing personal possessions for probate is short and clear: "You can also get a professional valuation for anything worth over £1,500." On form IHT407 (the schedule for household and personal goods), executors must list individual items of jewellery, vehicles, antiques, art, and collectibles valued at £1,500 or more. Items below that threshold can be grouped under a single "all other household goods" line.

The threshold seems straightforward, but it raises an immediate question: what counts as one item? Three Victorian rings worth £700 each are clearly three separate items, none triggering the rule. But what about a pair of matching Georgian candlesticks, a six-piece silver tea service, or a stamp collection of two thousand individual stamps? The answer depends on a body of valuation principle that HMRC and probate practitioners apply, and getting it wrong can leave the estate exposed.

The Natural Unit Principle

The foundational rule comes from Duke of Buccleuch v IRC [1967], a House of Lords case that established how property must be valued for tax purposes. The principle is that an asset should be valued in the form a willing buyer would naturally acquire it — its "natural unit" of sale.

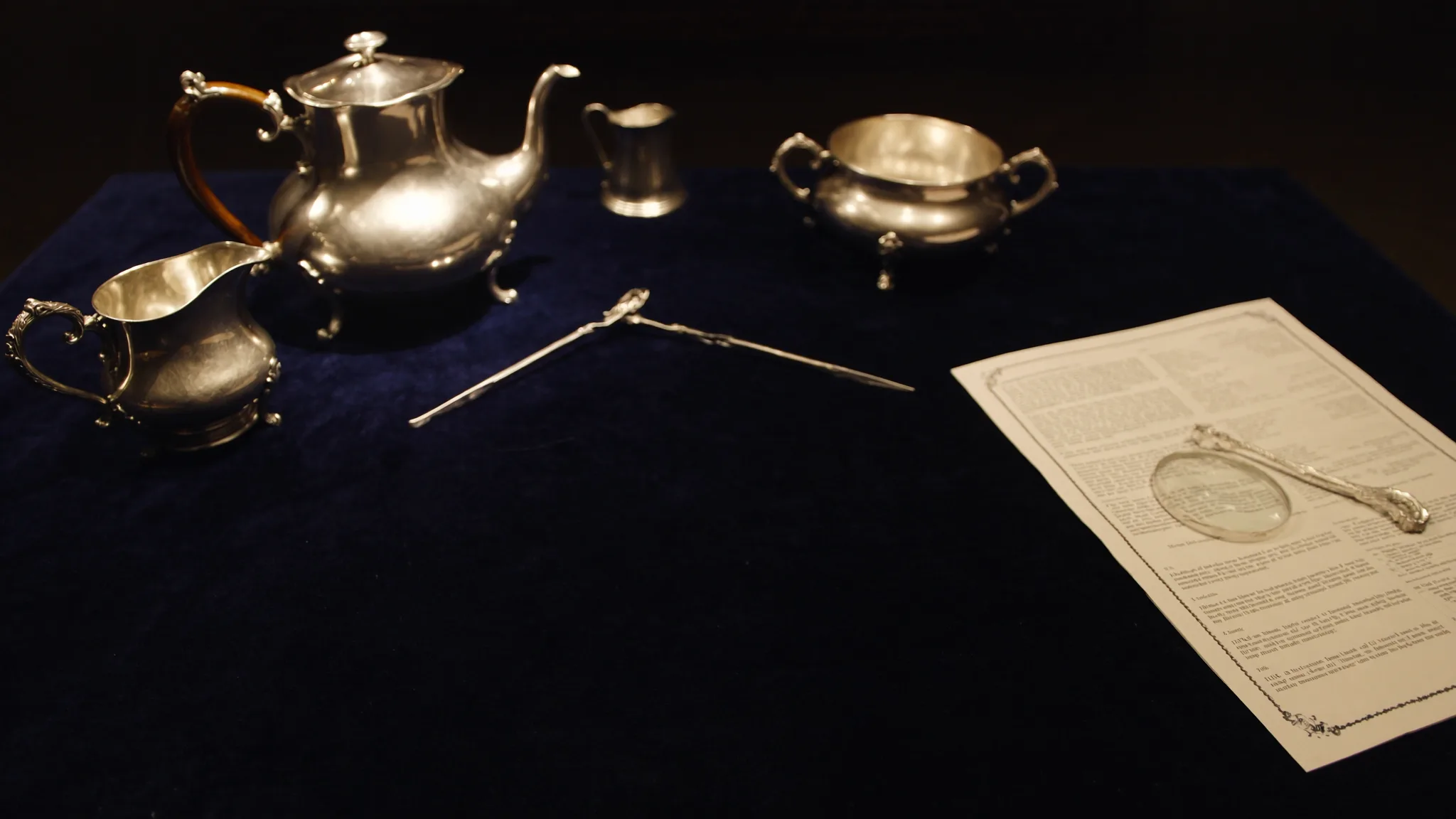

For chattels, this means matched sets, pairs, and suites are typically valued together rather than as their constituent pieces. A pair of antique candlesticks is more valuable as a pair than as two single candlesticks, because the market for matched pairs is stronger and the items lose value if separated. A complete six-piece tea service is worth more than the same pieces sold individually, because complete services are rare and command a premium.

In practice, this means a pair of items each worth £900 in isolation may be valued at £2,200 as a pair (a 22% set premium is typical for matched silver and ceramics). The set crosses the £1,500 threshold and must be professionally valued and listed individually on IHT407.

How Sets and Pairs Are Treated

The natural unit rule applies most clearly to objects designed and sold as sets or pairs. Common examples include:

- Pairs of candlesticks, vases, urns, mirrors, and chairs

- Silver tea services, coffee services, and dinner services

- Suites of furniture (a sofa with matching armchairs; a bedroom suite)

- Canteens of cutlery (silver, silver-plate, or designer steel)

- Sets of dining chairs (typically valued as a set of six, eight, or twelve)

- Matched pairs of paintings (pendant portraits, landscape pairs)

- Garniture sets (typically a clock with matching side ornaments)

How Collections Are Treated

Collections of similar items present a different question. A stamp collection, a wine cellar, a coin collection, a library of antiquarian books — each may contain hundreds or thousands of individual items, with most worth less than £1,500 but some specific items potentially worth far more.

HMRC's approach to collections is to look both at the collection as a whole and at its constituent parts. The whole collection is often valued for context (because a coherent collection can attract collectors prepared to pay a premium for the entirety), but individual items within it are also assessed against the £1,500 threshold and listed separately on IHT407 if they exceed it.

A wine cellar, for example, might contain three hundred bottles with an aggregate value of £45,000. Most bottles cost £50-£200 and would be reported under "all other household goods" if assessed individually. But if the cellar contains a 1982 Château Margaux worth £4,000 a bottle, those specific bottles must be listed individually on IHT407. The same logic applies to stamp collections (where a £20,000 Penny Black sits alongside £2 commemoratives) and coin collections.

For collections of broadly homogeneous items where no single piece exceeds £1,500, HMRC accepts a single grouped valuation supported by a specialist's report. Stamp dealers, numismatists, and wine specialists routinely provide these collective valuations.

IHT407 Reporting in Practice

Form IHT407 is the schedule executors use to report household and personal goods. It splits items into categories: jewellery, vehicles (including boats, caravans, and aircraft), antiques and works of art, collections, and "other" household goods.

The form's instructions are explicit. For jewellery: list individually any item valued at £1,500 or more. For vehicles: list each vehicle separately, regardless of value. For antiques and works of art: list individually any item valued at £1,500 or more. For collections (stamps, coins, books, wine): list individually any specific item worth £1,500 or more, and provide a total for the rest of the collection supported by a specialist valuation where the aggregate is significant.

The threshold for individual reporting is £1,500. The threshold for needing a professional valuation can sit lower — many practitioners advise professional assessment for any item the executor believes might be worth £500 or more, simply because the cost of being wrong (HMRC enquiry, penalty, executor liability) exceeds the cost of the valuation. HMRC themselves note that "anything worth over £1,500" can be professionally valued, which is permission rather than mandate, but the implication for executors handling marginal items is clear.

Edge Cases That Catch Executors Out

Several common situations cause confusion in practice. Knowing them in advance avoids costly mistakes.

- A pair of items where one is broken or lost. The remaining single item is valued as a single piece, not at half the pair value. A broken pair often loses 60-70% of the matched-pair value, and the surviving item must be valued at its actual single-item open market value.

- A set with one missing piece. A six-piece tea service missing the milk jug is usually valued as a five-piece "incomplete service" — typically at 50-65% of the complete value, depending on category and how distinctive the missing piece is.

- Matched but not original pairs. Two candlesticks of the same design but different dates of manufacture are usually valued individually, not as a pair, because the market does not treat them as a true matched pair.

- Sets that have been broken up across beneficiaries before valuation. The set is valued at its date-of-death value — which means the executor must value it as a complete set even if it is going to be split. The split only happens after probate.

- High-value items hidden within mundane categories. A "box of old jewellery" worth £200 by weight may contain a single Edwardian diamond brooch worth £8,000. Items must be assessed item-by-item for the threshold, not by container.

- Costume jewellery and unhallmarked pieces. Designer costume jewellery (Chanel, YSL, Trifari) can be worth thousands of pounds despite containing no precious metal. The £1,500 threshold applies regardless of material composition.

When in Doubt, Get a Professional Assessment

The cost of an initial professional opinion is modest. A qualified probate valuer can typically assess a household's personal goods in a single visit, identifying which items exceed or might exceed £1,500, which sets need treating as natural units, and which collections need specialist sub-valuations.

This initial assessment costs £100-£300 for most homes and protects the executor from the two costly failure modes: missed items that HMRC later challenges, and over-cautious valuations of every item that drive up valuation fees unnecessarily. The valuer's report becomes the executor's defensible position if HMRC raises questions about the IHT400 figures.

The valuation fee is itself deductible from the estate before Inheritance Tax is calculated, so the cost is borne by the estate rather than the executor personally.

Frequently Asked Questions

Do I need to value matching items as a set or individually?

If the items were designed and sold as a set, pair, or suite, they are normally valued together as their natural unit. A pair of antique candlesticks is valued as a pair; a six-piece tea service is valued as a service; matched dining chairs are valued as a set. The set value is often higher than the sum of the individual pieces, because complete sets command a market premium.

My father had a stamp collection. How is that treated for probate?

Stamp collections are typically valued in two parts. The collection as a whole is given an aggregate value supported by a specialist philatelist's report. Individual stamps within the collection worth £1,500 or more are listed separately on IHT407. The same approach applies to coin collections, wine cellars, and antiquarian book collections.

What if I do not know whether a single item is worth £1,500?

Get a professional opinion. Most probate valuers offer initial assessments that identify which items exceed the threshold, often as part of a single home visit covering the whole estate. The cost is modest (£100-£300 for typical homes) and is deductible from the estate before Inheritance Tax. The alternative — guessing wrong and triggering an HMRC enquiry — is significantly more expensive.

Does the £1,500 threshold apply to vehicles?

No — vehicles are listed individually on IHT407 regardless of value. This applies to cars, motorcycles, caravans, boats, and aircraft. The £1,500 threshold is for household goods, jewellery, antiques, and works of art. Vehicles each require their own line on the form.